Wall Street closed lower yesterday, but largely erased losses. Asia performed better and closed higher, partly on favorable figures from Alphabet and Microsoft. The futures therefore point to a higher opening for our main index: +0.6%.

The earnings season is now in full swing. There doesn’t seem to be a quiet Friday, because there are a number of important points that you need to pay close attention to today. In the early morning the Bank of Japan took an interest rate decision. Will there be an increase for the second time in a row? The market doesn’t think so, because the consensus is unchanged, as it is called. There was no surprise, because the interest rate remains at 0%.

Moreover, we also have to process a flood of company figures. Corbion, IMCD, Signify and Basic-Fit (all before the fair). Be sure to pay attention to Shell during the day, because sector peers TotalEnergies, Chevron and Exxon Mobil are all reporting figures. Or is that all? No.

You can also expect slight price pressure on the AEX today, because the ASML and ABN Amro shares will go ex-dividend at €1.75 and €0.89 respectively. Although ABN Amro (unlike ASML) is to a lesser extent an index heavyweight. Vopak (€1.50) and Wereldhave (€1.20) are also trading ex-dividend. If you would like to know more about the composition of the AEX and how much each share weighs, click here.

Core PCE Inflation (US)

The most important macro figure comes from America: the Core PCE inflation (at 2:30 PM). This is the inflation rate on which the Federal Reserve mainly bases its monetary policy. The latest inflation figures were on the high side. Economists expect core PCE inflation of 0.3% (MoM), similar to February. The annualized figure is expected to have cooled to 2.6% from 2.8% in February.

Regular PCE inflation is expected to be 0.3% on a monthly basis (the same as in February), but will rise to 2.6% on an annual basis (compared to 2.5% the month before). Another high score could be grist to the mill of stock market followers who do not expect a rate cut from the Fed for the time being. Disappointing economic growth and higher inflation would be a bad combination for stock markets.

CVC IPO

Another nice news is the IPO of CVC Capital Partners. The venture investor and partial owner of Douglas is aiming for a valuation of around $14 billion. This means that a share should cost between €13 to €15. But what happened yesterday afternoon?

That CVC wants to raise around €500 million more than the initial €1.8 billion that the investment company had in mind – including the over-allotment option. “Subscriptions below €14 per share will most likely remain unsuccessful,” the accompanying banks wrote. It has long been nice that the IPO was not canceled at the last minute again!

If the first price appears on the board within an hour, you can also participate as a private investor.

Here you can read Martin Crum’s analysis of this newcomer.

Figures Corbion, IMCD and Signify

AEX fund IMCD saw operational EBITA decline by 15% compared to a year ago. Earnings per share fell by 19% to €1.41 – compared to €1.74 in the same quarter last year.

In the first quarter of the year, the company achieved a gross profit of €295 million, equal to the same period last year on a constant currency basis. Free cash flow was €106 million, compared to €147 million in the first three months of 2023. Despite this, the company has successfully completed six acquisitions, including Valuetree and CJ Shah in India, Joli Foods in Colombia, RBD in China, Euro Chemo- Pharma/Biofresh in Malaysia and Gova in the Benelux.

Corbion has seen turnover and results decline both at core level and for the entire group in the first quarter of this year, but the shareholder will distribute a special dividend and will buy back its own shares.

Core turnover fell in the first quarter from €312.5 million to €300.9 million, an organic contraction of 2.8%. Total group turnover fell from €359.6 to €344.3 million, an organic decrease of 3.4%. Corbion’s cash flow amounted to €7.5 million positive.

Signify achieved less turnover than expected in the past quarter. The EBTIA margin was also disappointing. “In the first quarter, we saw improved momentum in our US Professional, OEM and Consumer businesses, while the market in China remained weak and the European Professional business was significantly below our expectations,” CEO Eric Rondolat said in a statement. on the numbers.

Signify recorded a 12.5% lower turnover of €1.5 billion last quarter, compared to €1.7 billion in the same period a year earlier. The EBITA margin fell from 8.9% to 8.3%. The bottom line was a net profit of €44 million, compared to €28 million a year earlier. The free cash flow also turned out better.

Wall Street

Wall Street closed lower, but some of the losses from earlier in the day were recovered. The S&P 500 ultimately fell 0.5% to 5,048.42 points, the Dow Jones index lost 1% to 38,085.80 points and the Nasdaq closed 0.6% lower at 15,611.76 points. On a macroeconomic level, attention was paid to the provisional growth figures for the first quarter in the US.

The US economy grew by 1.6% in the first three months of 2024. Economists expected growth of more than 2%. In the fourth quarter, growth was still 3.4%. Swissquote Bank stated that a disappointing growth figure is bad for the prospects of companies, but is favorable for an interest rate cut.

After the stock exchange closed, a small handful of companies reported their first quarter results. We are not talking about the least names: Alphabet, Microsoft, Intel and Snap. Who appears to be the best at first glance?

That appears to be Snap. After trading, the share price is 23.8% higher. Followed by Alphabet (+11.1%) and Microsoft (+4.1%). Intel ruins that party and is the bad apple. The numbers are clearly not popular and investors are unrelenting. Intel shares are trading 8.9% lower after hours.

Asia

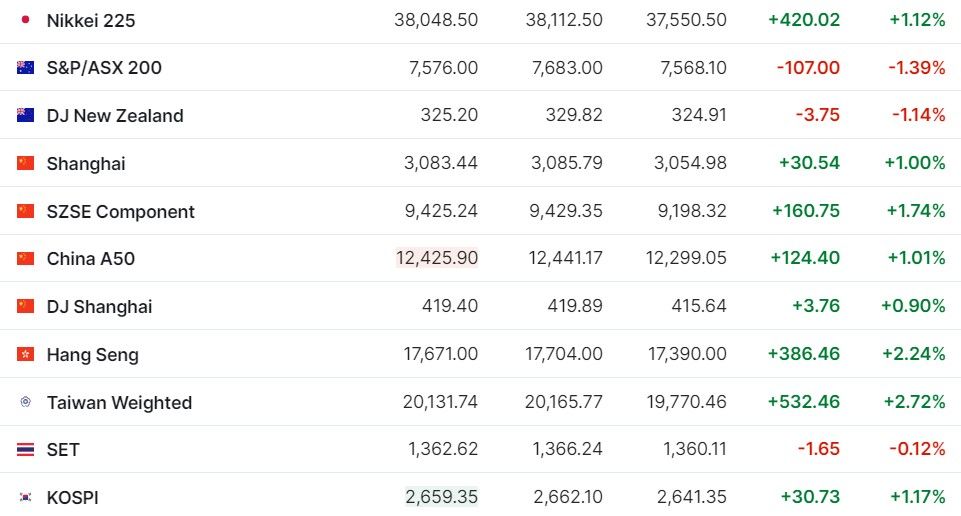

Asian stock markets were mainly in the green on Friday morning, ahead of US PCE inflation this afternoon. The leader was the Hang Seng index in Hong Kong with an increase of around 2%, while the stock exchanges in Tokyo, Seoul and Shanghai all gained around 1%. Sydney was the discordant with a loss. In response to the inflation figures and the interest rate decision, the yen weakened further against the dollar, reaching a new low this century. The dollar/yen stood at 156.20.

The state of affairs

- The AEX is expected to open higher.

- European futures point to a mostly higher open.

- Asia ended up mostly in the green.

- The CBOE VIX index (volatility) is trading at 15.37.

- The euro falls to $1.0728.

- The Dutch ten-year interest rate is 2.92%.

- The gold price rises by 0.3% to $2,339 per troy ounce.

- For a barrel of WTI oil you now pay $84.03.

- Bitcoin is trading at $64,303.

News

The most important news from ABM Financial News:

- 08:00 Basic-Fit records higher turnover with more than 4 million members

- 07:42 Lower turnover and results at Corbion

- 07:34 Turnover Signify disappoints

- 07:26 Flat sales and lower profits for IMCD

- 07:08 Asian stock markets are trading mainly higher

- 07:00 Bank of Japan leaves interest rates unchanged

- 06:55 European stock markets open in green

- 06:50 Stock market agenda: macroeconomic

- 06:49 Stock market agenda: foreign funds

- 06:48 Exhibition agenda: Dutch companies

- Apr 25 Alphabet pays out dividend for the first time

- Apr 25 Snap price jump after strong outlook

- Apr 25 Intel disappoints with AI sales

- Apr 25 Microsoft beats expectations

- Apr 25 Higher advertising revenue Alphabet

- April 25 Wall Street partly wipes away losses

- April 25 Stock market update: AEX on Wall Street

- Apr 25 Oil prices rise

- April 25 Wall Street is trading lower

- April 25 Shareholders’ meeting Heineken approves all agenda items

- April 25 Besi shareholders protest against remuneration report

- Apr 25 European stock markets fall as interest rates rise

- Apr 25 Airbus sees turnover and profit rise

- April 25 Annual meeting Fugro agrees on all points

Shorts

The AFM reports these shorts:

Agenda April 26, 2024

- 07:00 – Bank of Japan interest rate decision (unchanged; 0%)

- 07:00 – Corbion Q1 figures

- 07:00 – Signify Q1 figures

- 07:00 – IMCD Q1 figures

- 07:30 – Basic-Fit trading update Q1 and annual meeting

- 08:00 – Total Energies Q1 numbers

- 09:00 – ABN Amro €0.89 ex-dividend

- 09:00 – ASML €1.75 ex-dividend

- 09:00 – Vopak €1.50 ex-dividend

- 09:00 – Wereldhave €1.20 ex-dividend

- 09:00 – Acomo annual meeting

- 1:00 PM – AbbVie Q1 numbers

- 1:00 PM – Colgate-Palmolive Q1 numbers

- 1:00 PM – Chevron Q1 numbers

- 1:00 PM – Exxon Mobil Q1 numbers

- 2:30 PM – US personal spending and PCE inflation in March

- 4:00 PM – US consumer confidence (April)

And then this

BOJ does nothing

China unloved and increasingly excluded

Do you know it? A pilot project by Rheinmetall for innovative loading curbs in public spaces.

Huge surplus of electric cars from China.

Have fun and good luck today.

Tags: Premarket IMCD Corbion Signify Q1s PCE inflation afternoon

-

{kind=link}